TFSA vs. RRSP: How to choose the right one for you

Are you using the right accounts to save and achieve your financial goals? For Canadians, the Tax-Free Savings Account (TFSA) and Registered Retirement Savings Plan (RRSP) each offer unique strengths to support your savings strategy.

TFSAs, with their tax-free growth and ability to restore contribution room for withdrawals, are ideal for many different investors with different savings objectives. RRSPs, with their focus on retirement and tax deductibility of contributions, become increasingly beneficial as taxable income rises.

Knowing how and when to use these accounts can help you tailor them to your individual needs.

The RRSP: a cornerstone of retirement planning

Designed primarily for retirement, RRSPs provide tax advantages that reward long-term planning.

Contribution limits are based on 18% of your earned income from the previous year, up to an annual maximum ($32,490 for 2025).

- Reduce your tax bill: Contributions lower your taxable income. The higher your tax bracket, the greater your tax savings.

- Tax-deferred growth: Investment earnings, including interest, dividends, and capital gains, grow tax deferred.

- Tax-efficient retirement income: Withdrawals are taxed based on your applicable tax bracket determined by your income during retirement, which is often lower than in your peak earning years.

These features make RRSPs most effective for those with a long-term retirement focus, especially if you earn enough to benefit from the immediate tax deduction.

The TFSA: The ultimate in versatility

Unlike an RRSP, a TFSA can be used to save for almost any financial goal – retirement included.

The TFSA contribution limit for 2025 is $7,000, with unused contribution room carried forward. The cumulative limit for those eligible since 2009 is $102,000.

- No tax deduction: Contributions don’t reduce your taxable income, but earnings within a TFSA are completely tax-free.

- Tax-free withdrawals: Access your funds at any time without incurring taxes. Withdrawn amounts are even added back to your contribution room the following calendar year.

- No impact on government retirement benefits: Withdrawals don’t count as taxable income, preserving eligibility for programs like Old Age Security (OAS) and the Guaranteed Income Supplement (GIS).

You can use a TFSA to cover everything from immediate expenses to longer-term needs, all while keeping your savings growing tax-free.

What else do you need to think about?

Consider your tax bracket. Evaluate your tax bracket at the time you claim a deduction. If your tax bracket is higher when you claim than when you withdraw funds, an RRSP can serve as a powerful long-term retirement savings vehicle.

Assess your financial needs. The TFSA’s flexibility allows for easy access to savings for shorter-term needs, like an emergency fund. RRSPs are most suitable for longer-term investments earmarked for retirement.

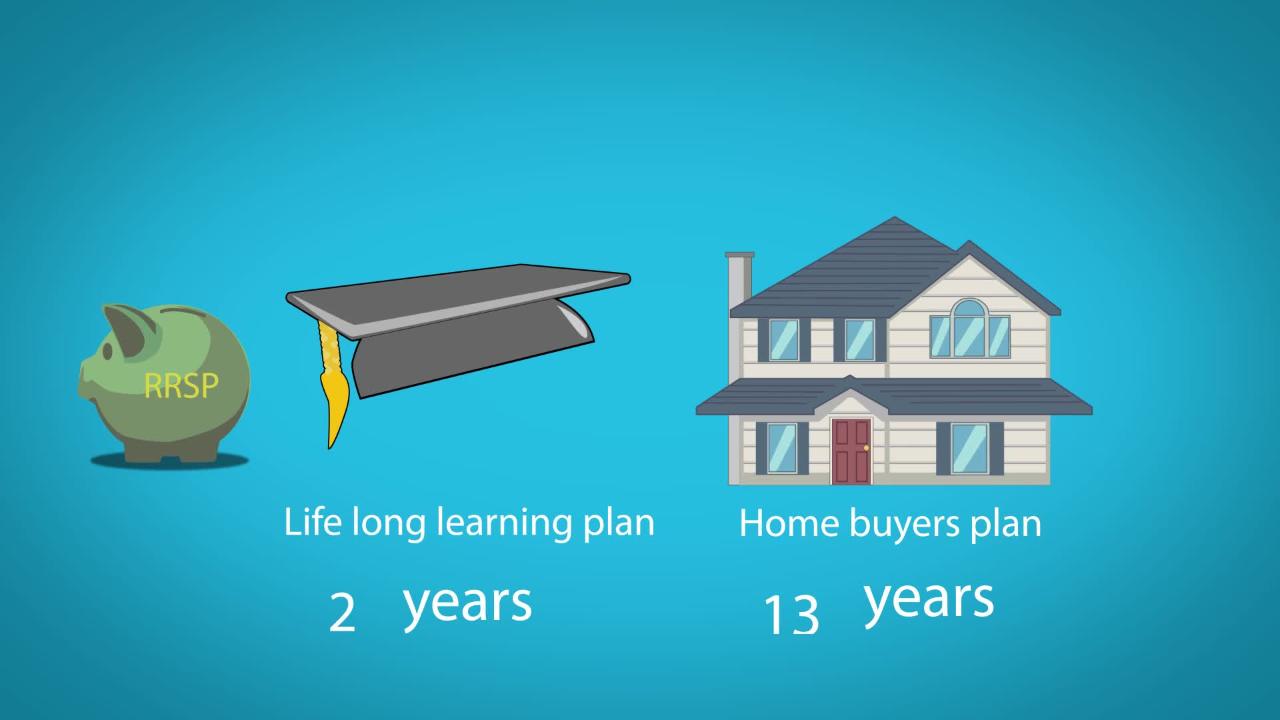

Planning a home purchase? If you qualify as a first-time homebuyer as defined by the Canada Revenue Agency (CRA), you can withdraw up to $60,000 from your RRSP under the Home Buyers’ Plan. In this case, although RRSPs are meant for retirement, they’re also a practical option for saving for a first house.

Impact on government benefits. If you’re eligible for income-tested federal retirement benefits and concerned that your income in retirement may reduce some or all of these benefits, consider directing your savings to a TFSA.

Making it work for you

At Manulife Wealth, we understand that no two financial journeys are alike. That’s why our advisors take the time to understand what matters to you. Whether you’re just starting out, building a nest egg, or preparing for life after work, we’ll create a plan that makes sense for where you are now and where you want to go next.

Talk to your Manulife Wealth advisor to enjoy the full benefit of your TFSA, RRSP, and everything along the way.

Comparing savings options

|

Registered Retirement Saving Plan |

Tax-Free Savings Account |

|---|---|---|

Minimum age to own |

No legal minimum¹ |

Yes – age 18² |

Maximum age to own |

Yes – end of year you turn age 71 |

No |

Annual contribution limit |

18% of your earned income from the previous year, up to a maximum amount (adjusted for certain pension amounts) |

Dollar amount per year, indexed to inflation ($7,000 for 2025 tax year) |

Carry-forward of unused contribution room |

Yes |

Yes |

Tax-deductible contribution |

Yes |

No |

Monthly penalty on excess contributions |

Yes – on excess at month-end. If excess is removed by the end of the month, penalty will not apply for that month |

Yes – on the highest amount of excess at any time during the month³ |

Investment options |

A variety of investments, such as stocks, bonds, GICs, mutual funds, segregated fund contracts, cash |

A variety of investments, such as stocks, bonds, GICs, mutual funds, segregated fund contracts, cash |

Tax-deferred/tax-free investment growth |

Yes – tax-deferred |

Yes – tax-free |

Taxable on withdrawal |

Yes – fully taxable |

No – tax-free, except for growth after death if no successor holder |

Withdrawals added to contribution room |

No |

Yes – in the following calendar year⁴ |

Withdrawals affect federal income-tested benefits and tax credits |

Yes |

No |

Tax-deferred/tax-free transfer to spouse on death |

Yes |

Yes – if successor holder. Otherwise, limited to fair market value at date of death |

Tax-deferred/tax-free transfer to non-spouse beneficiary on death |

No – fully taxable to deceased unless beneficiary is a dependent minor or disabled |

Yes – only investment income after date of death is taxable |

There is a lot of noise about TFSAs and RRSPs.

There is a lot of noise about TFSAs and RRSPs.

Important disclosure

This article was originally featured in Solutions magazine © 2020 Manulife.

Please note that only advisors who are qualified and approved financial planners can provide financial planning advise. Please check with your advisor.

Manulife Securities related companies are 100% owned by The Manufacturers Life Insurance Company (MLI) which is 100% owned by the Manulife Financial Corporation a publicly traded company. Details regarding all affiliated companies of MLI can be found on the Manulife Securities website www.manulifesecurities.ca. Please confirm with your advisor which company you are dealing with for each of your products and services.